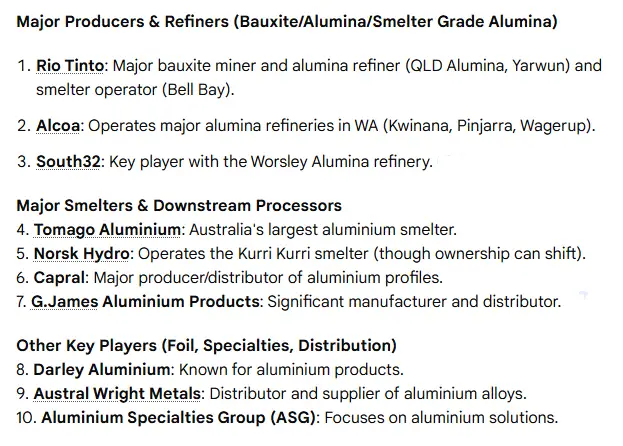

The Australian aluminium sector is dominated by a small group of large, vertically integrated players that control bauxite mining, alumina refining, primary aluminium smelting, and downstream fabrication. Rio Tinto, Alcoa, South32, and a handful of major joint-venture smelters and refiners together supply the bulk of Australia’s primary metal and alumina exports, while domestic extrusion and fabrication leaders such as Capral provide essential downstream capacity. Recent moves tied to energy costs, policy incentives, and refinery rationalisation have reshaped the competitive picture, making energy policy and decarbonisation the top strategic issue for every major operator.

Top 10 aluminium companies and operating entities in Australia

| Rank | Company / operating entity | Role in value chain | Notable Australian operations or assets | Why included |

|---|---|---|---|---|

| 1 | Rio Tinto (and its operating units) | Bauxite, alumina, smelting partner | Tomago Aluminium (major smelter), Boyne Smelters, Bell Bay, Queensland Alumina JV links | Largest combined footprint; multiple smelters and refineries; recent strategic moves. |

| 2 | Alcoa (Alcoa of Australia / Portland JV) | Bauxite, alumina, smelting | Pinjarra and Wagerup refineries, Portland aluminium smelter (JV) | Historic producer with integrated refinery and smelter operations, important export role. |

| 3 | South32 (Worsley Alumina) | Bauxite, alumina refining | Worsley Alumina integrated operation (major capacity) | One of Australia’s largest alumina refineries, major producer and employer |

| 4 | Tomago Aluminium (JV operator) | Primary aluminium smelter (ingots, billets) | Tomago smelter, Hunter Region, NSW | Country’s largest single smelter by capacity and local economic impact. |

| 5 | Boyne Smelters Ltd (BSL) | Primary aluminium smelter | Boyne Island smelter, Gladstone, Queensland | Second largest smelter by capacity, tight integration with Queensland Alumina supply. |

| 6 | Portland Aluminium (Alcoa-managed JV) | Primary aluminium smelter | Portland smelter, Victoria | Large regional employer; energy agreements shape long-term viability. |

| 7 | Bell Bay Aluminium (Rio Tinto / Pacific Aluminium) | Primary aluminium smelter | Bell Bay, Tasmania | Long-established smelter with strategic importance for Tasmania. |

| 8 | Queensland Alumina Limited (QAL) | Alumina refinery (JV) | Gladstone alumina refinery, major export volumes | One of the world’s larger alumina refineries; joint venture structure matters for supply. |

| 9 | Alumina Limited (legacy / corporate owner) | Alumina investment and historical owner of refineries | Note: acquired by Alcoa July 2024; included for historic significance and asset role | Until acquisition, major alumina investor; transaction changed ownership picture. |

| 10 | Capral Limited | Extrusions, downstream fabrication and distribution | National extrusion network, Aluminium Centres, product range for construction and industry | Largest Australian-headquartered extruder and major domestic fabricator. |

Notes: Several entries are corporate parents with multiple operating units. Ranking focuses on operational impact in Australia rather than global parent scale. Recent policy moves and ownership changes were incorporated. Key source material includes operator websites, national industry pages, and recent press coverage.

Short company profiles

Rio Tinto (operator presence through JVs and subsidiaries)

Rio Tinto controls major smelting and refining throughput through both majority ownership and joint ventures. Tomago, Boyne Island, and Bell Bay represent the primary aluminium smelting points linked to Rio Tinto or its partners. The company has been active in consolidating stakes in domestic smelters and negotiating energy contracts that determine each plant’s commercial viability. Recent reporting shows Rio Tinto’s strategic interest in keeping core smelters operational while navigating high energy prices.

Alcoa (Australia operations)

Alcoa runs large bauxite mines and alumina refineries in Western Australia and manages the Portland aluminium smelter in Victoria through a joint-venture structure. Alcoa’s Australian operations remain critical for supply into Asia and for local manufacturing; the company has undergone refinery rationalisation in recent years and continues negotiating power arrangements for smelter longevity.

South32 (Worsley Alumina)

South32’s Worsley Alumina is an integrated bauxite-to-alumina operation located in Western Australia. It is one of the largest single alumina refineries in the world by nameplate capacity and plays a central role in Australia’s alumina export profile. South32 regularly appears in industry coverage for production forecasts and permit-driven expansion plans.

Tomago Aluminium (site-level operator)

Tomago is Australia’s largest single smelter by nameplate capacity. The plant supplies ingots, billets, and slab products to regional markets and has a large regional economic footprint. Future operating choices for Tomago are heavily linked to energy costs and government policy support.

Boyne Smelters Ltd

Boyne Island smelter is a high-capacity plant fed by Queensland Alumina. Ownership has shifted over time toward a larger Rio Tinto stake, reflecting consolidation. Proximity to alumina supply makes its economics sensitive to both refinery production and power pricing.

Portland Aluminium

Portland is an Alcoa-managed JV smelter in Victoria. Securing long-term energy contracts has been central to recent announcements that aim to keep this plant competitive. Portland’s continued operations depend heavily on contract renewals and the cost of electricity.

Bell Bay Aluminium

Bell Bay in Tasmania supplies niche primary metal product volumes and supports local employment. Energy supply discussions with Hydro Tasmania and state authorities have been prominent in recent public reports.

Queensland Alumina Limited (QAL)

QAL is a major Gladstone refinery with a long operating history and global offtake. It remains one of the largest alumina refining operations in Australia and contributes heavily to alumina export tonnage.

Alumina Limited (historical investor)

Alumina Limited previously held material interests across the Australian alumina sector prior to acquisition by Alcoa in 2024. The acquisition reshaped asset ownership and clarified management lines for several refineries.

Capral Limited (fabrication and extrusions)

Capral is the leading Australian-headquartered extruder and national supplier of semi-fabricated aluminium products. Its network of extrusion presses and Aluminium Centres supplies construction, transport, and solar industries throughout the country. Capral’s domestic presence gives it strategic importance in the downstream market.

Also Read: Top 10 Aluminum Companies in The World.

Production capacity and ownership map

| Asset / operator | Product (aluminium or alumina) | Approx capacity (Mt or kt/year) | Ownership notes |

|---|---|---|---|

| Tomago Aluminium | Primary aluminium | ~590,000 t/year | Rio Tinto majority with Gove Finance and Hydro minority stakes. |

| Boyne Smelters Ltd | Primary aluminium | ~505,000 t/year | Rio Tinto majority JV, several Japanese partners. |

| Portland Aluminium | Primary aluminium | ~345,000 t/year | Alcoa-managed JV with CITIC and Marubeni partners. |

| Bell Bay Aluminium | Primary aluminium | ~178,000 t/year | Rio Tinto / Pacific Aluminium. |

| Worsley Alumina (South32) | Alumina | ~3.8 Mt/year | Majority South32; integrated bauxite mine and refinery. |

| Queensland Alumina (QAL) | Alumina | ~3.95 Mt/year | Independently managed JV led by Rio Tinto and partners. |

| Alcoa refineries (Pinjarra, Wagerup) | Alumina | Multiple Mt/year combined | Alcoa operations in WA; Kwinana curtailed/closed during recent rationalisation. |

| Capral (extrusion network) | Extruded products | Industrial capacity ~70,000 t/year extrusion press throughput | National extrusion capacity, multiple centres. |

Sources: operator statements, industry body figures, and recent press. Numbers are rounded to reflect publicly reported nameplate capacity and common industry references.

How Australia’s aluminium value chain functions

-

Bauxite mining: Bauxite is mined in Queensland, Western Australia, the Northern Territory, and Tasmania. Australia ranks among the world’s largest bauxite producers and supplies feedstock for local refineries and export markets.

-

Alumina refining: Bauxite undergoes the Bayer process at refineries that produce smelter-grade alumina. Australia’s alumina refineries represent a large export stream by tonnage.

-

Primary aluminium smelting: Alumina is smelted by electrolysis to metallic aluminium at smelters that are electricity intensive. Smelter economics hinge on low-cost, reliable power.

-

Fabrication and recycling: Extruders and fabricators convert primary metal and recycled aluminium into profiles, sheet, and specialised articles. Domestic capacity supports construction, transport, and renewable-energy supply chains.

Australian aluminium market snapshot

| Metric | Latest published figure or range | Source |

|---|---|---|

| Primary aluminium production (Australia, 2024) | ~1.58 million tonnes | Australian industry body report. |

| Alumina production (Australia, 2024) | ~17.54 million tonnes produced; ~14.73 Mt exported | Australian alumina industry summary. |

| Number of major alumina refineries | Five operating refineries (major players listed) | Industry association. |

| Main export markets | Asia region (China, Japan, South Korea), global metal markets | Export patterns tracked by port data and industry reports. |

Interpretation: Australia plays an outsized role in global alumina exports while primary aluminium output is concentrated in a small number of energy-intensive smelters. This structure makes domestic outcomes highly sensitive to policy on energy, decarbonisation incentives, and international metal demand.

Key factors that influence aluminium prices in Australia

| Factor | How it moves price or supply | Short explanation |

|---|---|---|

| Global LME price and demand | Direct feed-through for export contracts | Global primary aluminium prices determine revenue rates for primary producers. |

| Electricity cost | Major operating expense for smelters | Smelters consume very high electricity per tonne; price swings have immediate profit impact. |

| Alumina supply and bauxite quality | Affects smelter feedstock price and smelter throughput | Refinery outages or bauxite grade shifts change marginal costs. |

| Exchange rates (AUD/USD) | Exports priced in dollars affect revenue in local currency | Strong AUD reduces export revenue in AUD terms; weak AUD boosts it. |

| Freight and logistics | Shipping cost spikes change delivered cost and competitiveness | Port congestion or freight rate hikes change landed prices. |

| Carbon policy and credits | Creates cost for carbon-intensive routes or premium for green metal | Policy incentives such as the Green Aluminium Production Credit change long-run competitiveness. |

| Trade policy and tariffs | Can shift supply/demand balance quickly | Regional trade limits or anti-dumping actions alter market access. |

Energy and policy give Australia a unique risk profile because smelters are long-lived facilities that require cheap electricity to compete with producers in other regions. Recent government programs intend to alter that calculus.

Five- to ten-year outlook — scenarios and implications

| Scenario | Likelihood (expert view) | What it means for major players |

|---|---|---|

| Energy transition with supportive policy (Green credits implemented, new renewables scale-up) | Moderate to high | Smelters gain pathways to retrofit for low-carbon electricity; operators who secure contracts remain viable. Government support will shape which plants continue. |

| Continued high energy costs with weak policy support | Moderate | Some smelters may be mothballed or face closure; downstream fabrication shifts overseas. Operators with captive renewable supply fare better. |

| Strong global demand and price spike | Low to moderate | Higher margins make current plants profitable, but long-term energy and carbon constraints persist. |

| Consolidation and vertical integration | High | Expect further M&A, joint-venture rebalancing to secure feedstock and market access; prior acquisitions have already reshaped ownership. |

| Premium green aluminium market development | Moderate | Australian producers who decarbonise can capture higher-value contracts in automotive and electronics sectors. Government credits and certification schemes will be crucial. |

Overall expert view: Policy choices and power contracts will determine which large sites remain open beyond 2028 to 2035. Facilities with clear decarbonisation roadmaps or competitive long-term power deals will have the edge.

2024-2033(USD Billion)

Practical implications for different stakeholders

-

Buyers (manufacturers, wholesalers): Prioritise long-term sourcing agreements with operators who have committed to stable energy sourcing. Green aluminium premiums will emerge; include sustainability clauses.

-

Suppliers (energy, reagents, equipment): Energy-storage and renewable integration solutions represent growth markets; maintenance and retrofit services will be in demand.

-

Investors: Look for operators with secure long-term power agreements or credible transition plans; regulatory risk around plant closure is real.

-

Policy makers: If preserving regional jobs is a goal, policy must align energy provisioning with decarbonisation targets while avoiding costly distortions.

Sources, methodology and final notes

Major sources used for this briefing include operator websites and press releases (Rio Tinto, Alcoa, Tomago), national industry association data, and recent reporting by reputable news outlets and government pages. Key references that support the most important facts in this article are listed below:

-

Australian aluminium industry profile and recent production/export numbers.

-

Tomago, Boyne, Portland and Bell Bay operational details and capacity figures.

-

South32 Worsley Alumina operation overview and capacity references.

-

Alcoa Australia site information and refinery updates.

-

Government policy on decarbonisation support for aluminium, Green Aluminium Production Credit.