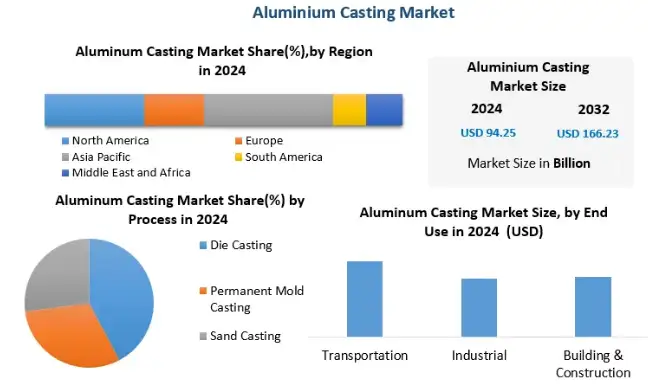

The global aluminum casting market is currently valued at approximately USD 78.5 billion as of closing estimates for 2024. Financial projections and industrial data indicate a robust growth trajectory with a Compound Annual Growth Rate (CAGR) of 6.4% to 7.1% over the next eight years. By the end of 2032, the total market valuation is expected to surpass USD 132 billion. This growth is primarily fueled by the aggressive shift toward lightweight components in the automotive sector, specifically for Electric Vehicles (EVs), alongside rising demand in the construction and aerospace sectors. Asia-Pacific remains the dominant region, commanding over 40% of the global market share, driven by manufacturing powerhouses like China and India.

Current Market Valuation and Economic Impact

Understanding the sheer scale of the aluminum casting industry requires looking beyond just the revenue figures. The volume of production is equally critical. In 2024, the global production volume exceeded 26 million metric tons. This figure represents a massive logistical and industrial operation involving raw bauxite mining, alumina refining, and the complex casting processes that follow.

The economic impact extends into secondary markets. The demand for recycled aluminum (secondary aluminum) is outpacing primary aluminum in casting applications due to lower energy costs and environmental regulations. For companies like AdTech, which specializes in molten metal purification and filtration, this market expansion signals a critical need for higher quality control. As casting volumes increase, the cost of scrap due to impurities becomes a significant liability for foundries. The market is not just growing in size; it is growing in complexity. Foundries are under pressure to deliver thinner, stronger, and more defect-free castings than ever before.

The Role of CAGR in Long-Term Planning

A CAGR of roughly 6.5% might seem moderate compared to the tech sector, but in heavy industry, this represents massive capital investment. It implies that foundries must expand their capacity by nearly 50% over the next decade.

This growth is not linear. We anticipate a steeper curve between 2026 and 2028 as major automotive OEMs phase out internal combustion engine platforms in favor of EV architectures. These architectures utilize large-scale aluminum castings (often called gigacastings) to replace multiple steel parts. This structural shift fundamentally alters how we calculate market potential. It is no longer about selling pounds of metal; it is about selling structural integrity.

Market Segmentation by Casting Process

The aluminum casting market is not a monolith. It is divided into several distinct processes, each serving different industrial needs. Understanding these distinctions is vital for grasping where the money is really flowing.

Die Casting: The Market Leader

Die casting dominates the sector, accounting for approximately 60% to 65% of the total revenue. The efficiency of High-Pressure Die Casting (HPDC) makes it the preferred method for mass-producing automotive parts like engine blocks, transmission cases, and increasingly, battery housings. The speed at which molten aluminum can be injected into steel molds allows for high-volume production with tight tolerances.

Permanent Mold Casting

This process holds a smaller but significant share. It is used where higher strength is required than standard die casting can offer. Applications include wheels and suspension components. The market for permanent mold casting is growing steadily as safety standards in automotive and aerospace become stricter.

Sand Casting

While slower and less precise than die casting, sand casting remains vital for low-volume, massive components. This segment is seeing slower growth but retains a stronghold in specialized machinery and heavy equipment manufacturing.

Table 1: Global Market Share by Casting Process (Estimated 2024)

| Casting Process | Market Share (%) | Key Applications | Primary Growth Driver |

| Die Casting (HPDC/LPDC) | 63.5% | Engine blocks, EV battery trays, Housings | Automotive EV Production |

| Permanent Mold | 18.2% | Wheels, Suspension knuckles | Strength/Weight Ratio Needs |

| Sand Casting | 12.1% | Heavy machinery, Prototypes | Industrial Equipment |

| Others (Squeeze, Lost Foam) | 6.2% | Specialized Aerospace, Defense | High-Performance Alloys |

Regional Analysis: Asia-Pacific Dominance

The geographical distribution of the aluminum casting market is heavily skewed. The Asia-Pacific (APAC) region is not just a participant; it is the engine of the global industry.

China and India

China accounts for the largest individual national market share globally. The relentless expansion of Chinese infrastructure, combined with its status as the world’s largest automotive manufacturing hub, drives this demand. India is following a similar trajectory, with government incentives pushing for increased domestic manufacturing in the defense and automotive sectors.

North America and Europe

These regions are mature markets. Growth here is not driven by volume expansion but by technological replacement. The US and Germany are leading the charge in adopting “Green Aluminum”—metal produced with renewable energy. This shift influences market value more than volume, as low-carbon aluminum commands a price premium.

Table 2: Regional Market Growth Projections (2025–2030)

| Region | 2024 Valuation (USD Billion) | Projected CAGR | Key Industry Focus |

| Asia-Pacific | $34.5 | 7.8% | Automotive, Infrastructure, Electronics |

| North America | $18.2 | 5.4% | Aerospace, EV Transition, Defense |

| Europe | $16.9 | 5.1% | Sustainability, Premium Automotive |

| Rest of World | $8.9 | 4.8% | Construction, Oil & Gas |

The Automotive Catalyst: EVs and Lightweighting

You cannot discuss the size of the aluminum casting market without analyzing the automotive sector. It is the single largest end-use segment, consuming over half of all aluminum castings produced globally.

The Lightweight Imperative

Electric vehicles are heavy due to their battery packs. To maximize range, manufacturers must reduce the weight of the chassis and body. Aluminum is the solution. It is one-third the weight of steel. Replacing heavy steel components with aluminum castings is the most effective way to offset battery weight.

Gigacasting Trends

Tesla introduced the concept of “Gigacasting,” where massive aluminum die-casting machines produce entire rear or front underbodies in a single shot. This eliminates hundreds of robots and welders. Other manufacturers like Toyota, Volvo, and Volkswagen are adopting similar strategies. This trend requires high-purity aluminum alloys. Even microscopic inclusions can cause a massive casting to fail, leading to expensive scrap. This is where AdTech’s expertise in molten metal filtration becomes an industry necessity rather than just an option.

AdTech Solutions in a Growing Market

As the market expands, the tolerance for error shrinks. High-performance castings for aerospace and EVs demand metal cleanliness levels that were previously unnecessary for general industrial parts.

The Cost of Impurities

In the casting process, hydrogen gas and non-metallic inclusions (oxides) are the enemies. If the aluminum casting market is worth $78 billion, the “cost of poor quality” (scrap and rework) is estimated to be billions of dollars annually. Foundries lose profit margins when castings fail X-ray inspection.

Ceramic Foam Filters and Degassing

AdTech provides the technology to capture these impurities. Our Alumina Ceramic Foam Filters are engineered to withstand high temperatures and physically trap debris from the molten stream. Furthermore, degassing units remove dissolved hydrogen, preventing porosity. As the market grows, the demand for these consumables grows in parallel. A larger market means more metal melted, which means more filtration is required to ensure that metal is usable.

Supply Chain Dynamics and Raw Materials

The supply chain feeding the aluminum casting market involves a mix of primary aluminum smelters and secondary refiners.

Primary vs. Secondary Aluminum

Primary aluminum is energy-intensive to produce. However, secondary (recycled) aluminum requires only 5% of the energy needed to produce primary aluminum. Consequently, the secondary aluminum casting market is expanding faster than the primary sector. This aligns with global ESG (Environmental, Social, and Governance) goals.

Volatility in Raw Material Costs

The market size is also influenced by the price of aluminum on the London Metal Exchange (LME). Geopolitical tensions, energy prices in Europe, and mining policies in nations like Guinea (a major bauxite source) cause fluctuations. When aluminum prices rise, the total market valuation increases, even if production volume remains flat.

Technological Advancements Driving Value

The market is not static; it is evolving through technology.

Simulation and Digital Twins

Modern foundries use advanced solidification simulation software to predict defects before pouring metal. This digital adoption increases the value provided by casting houses, allowing them to charge for engineering services, not just raw metal.

New Alloy Development

Standard A380 or A356 alloys are being supplemented by new, proprietary mixes designed for high conductivity or extreme heat resistance. These specialized alloys command higher market prices, contributing to the overall growth of the market size.

Challenges Restraining Market Growth

Despite the positive outlook, several factors could slow the expansion.

-

High Initial Capital: Setting up a modern die-casting facility requires millions in investment.

-

Energy Costs: Melting aluminum requires vast amounts of electricity and natural gas. In regions with volatile energy prices, foundries struggle to maintain margins.

-

Competition from Composites: In some high-end applications, carbon fiber composites compete with aluminum for lightweighting, though aluminum retains the cost advantage.

Future Outlook and Strategic Predictions (2025–2032)

Looking ahead, the aluminum casting market will undergo a consolidation phase. Smaller, less efficient foundries will struggle to meet the strict environmental and quality standards demanded by global OEMs.

We predict a rise in “Mega-Foundries” located near automotive assembly plants to reduce logistics costs. Furthermore, the integration of Industry 4.0—smart sensors, automated pouring, and real-time quality monitoring—will become standard. For AdTech, this means our role will evolve from a material supplier to a partner in process optimization, ensuring that the molten metal quality matches the sophistication of the casting machinery.

Table 3: Key Market Drivers and Inhibitors

| Driver/Inhibitor | Impact Level | Description |

| EV Adoption | High (Positive) | Urgent need for weight reduction drives aluminum usage. |

| Recycling Trends | Medium (Positive) | Increased use of secondary aluminum lowers material costs. |

| Energy Prices | High (Negative) | Rising electricity costs squeeze foundry margins. |

| Magnesium Competition | Low (Negative) | Magnesium is lighter but more expensive and harder to cast. |

Conclusion: The AdTech Perspective

The question “How big is the aluminum casting market?” yields a multi-billion dollar answer, but the nuance lies in quality rather than just quantity. With a valuation pushing toward $132 billion by 2032, the opportunity is immense. However, this growth is reserved for those who can solve the technical challenges of porosity, shrinkage, and mechanical failure.

AdTech stands at this intersection. By providing the essential filtration and purification technologies, we enable the casting industry to meet the rigorous demands of the future. The market is big, but the winners will be those who focus on the microscopic details that ensure structural integrity.

Global Aluminum Casting Market: Trends & Analysis 2026

1. What is the current global value of the aluminum casting market?

2. What is the projected CAGR for the aluminum casting industry?

3. Which industry is the largest consumer of aluminum castings?

4. How does the rise of Electric Vehicles (EVs) impact the market size?

5. What is the difference between primary and secondary aluminum in this market?

6. Why is Asia-Pacific the largest market for aluminum casting?

7. What role does AdTech play in the aluminum casting market?

8. Is aluminum die casting better than sand casting?

9. What are the main challenges facing the aluminum casting market?

- Raw Material Volatility: Fluctuating global prices for bauxite and energy.

- Energy Consumption: The high cost of maintaining melting temperatures.

- Sustainability: The pressure to achieve “Net Zero” carbon emissions across the production chain.

10. Will magnesium replace aluminum in the casting market?

Detailed Analysis of Process Variables affecting Market Size

To further understand the valuation, we must look at the variables affecting production costs and sales prices. The market size is not just a function of demand but also of the value added during the process.

The Shift to Structural Castings

Historically, aluminum castings were used for non-structural parts (brackets, housings). Today, the market value is being boosted by “structural castings”—parts that form the frame of a car. These parts require heat treatment (T5, T6 processes) and vacuum die casting technology to prevent air entrapment. This advanced processing adds significant value to the final product, inflating the overall market revenue figures.

Impact of Scrap Rates on Market Efficiency

If a foundry has a scrap rate of 10%, that represents 10% of energy and labor wasted. In a $78 billion market, billions are lost to inefficiency. AdTech’s focus on filtration technology directly addresses this economic loss. By reducing inclusions, we help foundries lower their scrap rates, effectively increasing their profitable output without increasing their melting costs. This efficiency gain is a hidden driver of market profitability.

Investment in Automation

The labor shortage in manufacturing hubs like the US and Europe is forcing foundries to invest in robotics. Automated cells for ladling, spraying, and extraction are becoming standard. While this increases the initial capital required to enter the market, it stabilizes long-term production costs, making the market more resilient to labor fluctuations.

Material Science: The Foundation of Market Growth

The chemistry of the metal dictates the application. The market size is partly driven by the development of premium alloys.

Al-Si-Mg Alloys

The workhorse of the industry is the Aluminum-Silicon-Magnesium family (like A356). Silicon provides fluidity (castability), while magnesium provides strength after heat treatment. Research into optimizing these ratios continues to expand the applications for aluminum casting, allowing it to take market share from steel fabrications.

Recycling Friendly Alloys

A major trend is the development of alloys that are more tolerant of impurities found in scrap metal. Creating high-performance parts from lower-grade recycled input is the “holy grail” of the industry. This capability allows foundries to manage costs better and protects the market from raw material shortages.

Strategic Recommendations for Industry Players

Based on current market data and forecasts, we offer the following strategic perspectives for stakeholders in the aluminum casting ecosystem.

Focus on Niche High-Performance Segments

Commodity casting (simple brackets, handles) is a race to the bottom on price. The real value growth is in complex, pressure-tight, and structural components. Foundries should invest in the technology required to produce these high-margin parts.

Secure Supply Chains via Recycling

Reliance on primary aluminum creates exposure to geopolitical price shocks. Integrating in-house recycling capabilities or securing long-term contracts for secondary ingot is a prudent hedge.

Adopt Advanced Filtration

As emphasized throughout this analysis, melt quality is non-negotiable for future growth sectors like EV and Aerospace. Utilizing AdTech’s advanced ceramic foam filters and fluxing agents is a cost-effective method to upgrade metal quality immediately without massive capital equipment expenditure.

By aligning with these trends—lightweighting, sustainability, and quality assurance—companies can capture a significant portion of the $132 billion opportunity that lies ahead. The aluminum casting market is not just getting bigger; it is getting smarter, cleaner, and more integral to the global economy.